Automotive Supply Chain Logistics in Southern Africa

June 29, 2026

Read the story

Please submit your details below and one of our logistics experts will reach out within one business day. Thank you.

South Africa's automotive industry is bigger and more globally connected than most people outside the sector realize. According to NAAMSA, in 2025, it exported a record 414,268 vehicles to 109 countries, generating automotive export earnings of R291 billion.

It accounts for 22.6% of South Africa's total manufacturing output and is the only country on the continent with a fully integrated automotive value chain, covering vehicle assembly, component manufacturing, catalytic converters, tyres, and transmission components.

That scale creates a logistics challenge that is both complex and consequential. Getting the right parts to assembly plants on time, moving finished vehicles to export markets efficiently, and managing the supply chains of a growing regional automotive market all require logistics infrastructure that is under significant development pressure across Southern Africa.

Automotive supply chain logistics connects the people who make vehicles and parts with the people and places that need them. Three distinct flows run through that connection:

● Inbound logistics covers raw materials and components moving into manufacturing plants

● Finished vehicle logistics covers completed vehicles moving out to dealers and export markets

● Aftermarket parts distribution covers replacement parts moving through dealer and service networks

Each flow has its own requirements, its own vulnerabilities, and its own cost structure. In vehicle manufacturing, where assembly lines run on just-in-time schedules, those requirements are unforgiving. A component that arrives late or not at all has immediate consequences on the production floor.

Finished vehicles need to move quickly from the plant to avoid tying up working capital. And parts distribution networks need to be responsive enough to keep vehicles on the road across a continent where distances are large, and infrastructure is uneven.

South Africa manufactures and exports at scale. The rest of Southern Africa buys. That split defines the regional automotive supply chain and shapes the logistics flows that run through it.

According to NAAMSA's 2026 Automotive Trade Manual, South Africa accounted for 50.3% of Africa's total vehicle production and 46.5% of total vehicle sales on the continent in 2025. Behind those figures sit decades of policy support through the Automotive Production Development Program, which has brought Toyota, Volkswagen, BMW, Mercedes-Benz, Ford, and Isuzu to a single country on a continent where integrated automotive manufacturing is otherwise absent.

Namibia, Botswana, Zambia, and Mozambique all depend on imports to meet domestic vehicle demand, with South Africa as the primary regional source for most categories. The logistics of supplying those markets, moving finished vehicles across borders and through ports that were not all designed with automotive distribution in mind, is where much of the complexity in regional automotive logistics sits.

The import picture is also changing within South Africa itself. According to NAAMSA, fifteen different Chinese vehicle brands were operating in the South African domestic market in 2025, up from eight in 2024, with more expected in 2026. Chinese brands are gaining share at the entry-level and small car segments, creating new logistics flows from Asian manufacturing hubs that were not part of the market a few years ago.

Southern Africa's automotive sector is at a point of transition. The established manufacturing base in South Africa is navigating a global shift toward new energy vehicles while defending its position in traditional export markets. The broader regional market is growing as urbanization, rising incomes, and improved road infrastructure increase vehicle ownership rates.

The opportunities are real, but there are constraints. Road infrastructure in many parts of the region still limits vehicle distribution. Dealership networks outside South Africa's major urban centers are thin. And the logistics infrastructure required to support an expanding automotive market, including vehicle processing centers, bonded storage, and efficient port handling, is still developing.

The policy environment is improving. The adoption of AfCFTA's automotive rules of origin has opened up more market access opportunities for South African vehicle exports across the continent. That is a significant development for an industry that exported only 35,371 vehicles into the rest of Africa in 2025, compared to 332,695 to Europe.

South Africa's position as the continent's automotive hub rests on several foundations that no other African country currently replicates:

● Seven OEM assembly plants producing vehicles for both domestic and export markets

● An established component manufacturing sector supplying both domestic assembly and export customers

● Long-standing Economic Partnership Agreements with the EU and UK that provide preferential market access

● The Automotive Production Development Programme, which provides production incentives that underpin investment decisions

● Port infrastructure at Durban and Port Elizabeth is capable of handling vehicle exports at scale

According to NAAMSA's chief trade and research officer, Norman Lamprecht, South Africa's automotive industry is export-oriented, relying heavily on trade agreements to sustain export volumes and competitiveness. That dependency is both a strength and a vulnerability: record exports in 2025 were achieved despite a significant fall in US-bound volumes following new American tariffs, offset by growth in European markets.

The four markets immediately north and east of South Africa represent different stages of automotive market development and different logistics challenges.

Namibia is a small but relatively well-developed vehicle market served primarily through Walvis Bay and direct road links to South Africa. The Trans-Kalahari Corridor gives it reasonably straightforward access to regional supply, making it one of the less logistically complicated markets in the region.

Botswana punches above its weight as a vehicle market, given its population size, supported by relatively high per capita income and strong vehicle ownership rates. Its landlocked status means all imports travel by road from South Africa, which means Botswana's automotive supply chain is directly exposed to corridor performance on the N1 and N14 routes.

Zambia is a growing market where Chinese brands have moved in quickly alongside established Japanese and South African names. Getting vehicles into Zambia means long road or rail hauls from Durban or Dar es Salaam, and border crossings that add both time and cost to every movement.

Mozambique is earlier in its automotive development, but a growing economy and active infrastructure investment are generating demand, particularly for commercial vehicles. Beira and Maputo both receive vehicle imports, serving different distribution catchment areas as roads improve and inland connectivity develops.

For years, the African Continental Free Trade Area promised to reshape automotive trade across the continent. According to NAAMSA, the adoption of automotive rules of origin under AfCFTA has opened up new market access opportunities for South Africa's vehicle exports across Africa. For an industry that sent only 35,371 vehicles to the rest of Africa in 2025, compared to 332,695 to Europe, the continent represents significant untapped potential.

The practical implications for logistics are significant. If AfCFTA delivers on its automotive trade potential, vehicle flows between South Africa and other African markets will increase. That means more finished vehicle logistics on regional corridors, more parts distribution into markets that currently have limited supply chain infrastructure, and more demand for bonded vehicle storage and processing facilities at key ports and distribution points.

According to Financial Mail, South African vehicle exports to the rest of Africa surged 36.4% in 2025, reaching 35,371 units. That growth rate, if sustained, points to a regional market that could become considerably more significant for the South African automotive industry than it is today.

South Africa's assembly plants depend on a continuous supply of components from both domestic and international sources. According to NAAMSA, imports of original equipment components by the seven domestic OEMs reached R151 billion in 2025. The majority of these components arrive through Durban and Port Elizabeth, move through customs clearance, and are delivered to assembly plants on schedules that leave little room for delay.

The inbound logistics challenge has several dimensions:

● Just-in-time delivery requires precise scheduling and reliable transit times that South Africa's logistics infrastructure does not always support

● Component sourcing concentration in specific geographies, particularly Germany, Japan, and increasingly China, creates exposure to disruptions at origin or in international shipping

● Customs clearance efficiency at entry ports directly affects the cost and reliability of component supply

● Road and rail performance on the corridors connecting ports to assembly plants affects the final leg of a supply chain that may have traveled halfway around the world

Moving completed vehicles from the assembly plant to market is a distinct logistics challenge from moving components. Vehicles are high-value, damage-sensitive cargo that requires specialist handling, transport, and storage.

Finished vehicle logistics has its own specialist infrastructure that sets it apart from general cargo handling. Vehicles are high-value, damage-sensitive, and need to move through a specific sequence of handling stages before they reach a buyer.

In Southern Africa, that sequence typically involves:

● Vehicle Processing Centers, where vehicles are inspected, prepared, and allocated before distribution begins

● Roll-on/roll-off vessel operations for exports, requiring dedicated RoRo berths and marshaling yards at port

● Car carrier transport for domestic and regional distribution by road

● Bonded storage at import markets for vehicles awaiting customs clearance

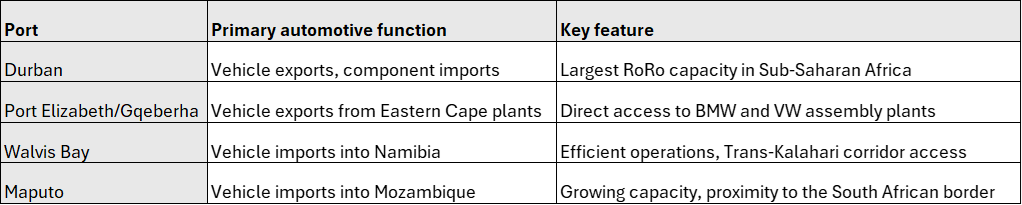

Durban handles the bulk of South Africa's vehicle export volumes, with RoRo connections to major shipping lines serving Europe and other markets. Port Elizabeth, now Gqeberha, serves the Eastern Cape assembly plants. Walvis Bay and Maputo handle vehicle imports into Namibia and Mozambique, each with different port infrastructure and inland distribution challenges to navigate.

The global automotive industry is transitioning toward electric vehicles, and that transition creates new supply chain requirements that Africa's logistics networks are only beginning to address.

EV supply chains differ from conventional automotive logistics in several important ways:

● Battery supply chains require lithium, cobalt, and copper from African mines, creating a supply chain loop that connects Southern African mineral producers to global battery manufacturers and back to African vehicle markets

● Charging infrastructure is a prerequisite for EV adoption that most African markets currently lack at any meaningful scale

● Skilled technician networks for EV servicing and maintenance are significantly thinner than for conventional vehicles

● Battery storage and handling at ports and distribution points require different facilities and safety protocols from conventional automotive parts

South Africa's position in the EV supply chain is potentially significant from both sides. As a producer of the critical minerals that EV batteries require, and as the continent's primary vehicle manufacturing and distribution hub, it sits at a strategic intersection. According to NAAMSA, South Africa's vehicle production base needs to align with the technology shift of global value chains to ensure the country remains part of the global supply network.

The shift to EVs also changes what needs to come in. Battery packs and EV-specific components require specialist handling, and in many cases, they attract different customs classifications and safety protocols from the parts they replace. For logistics operators used to handling conventional automotive cargo, that is a learning curve with real operational implications.

Road freight dominates the distribution of vehicles and automotive parts across Southern Africa. Car carriers move finished vehicles from assembly plants to dealerships and ports. Parts are distributed by road from distribution centers to dealer networks across the region.

Road freight for automotive cargo faces the same infrastructure constraints that affect all road logistics in Southern Africa: variable road quality on regional corridors, border crossing delays on multi-country movements, and the cost and reliability challenges that come with long-distance transport on infrastructure under pressure from heavy vehicle use.

Rail plays a limited but potentially growing role in automotive logistics in South Africa. Components moving from Durban port to inland assembly plants, and finished vehicles moving from assembly plants to regional distribution points, are candidates for rail if the service is reliable enough to support just-in-time schedules.

The reliability constraint has been the central problem. Transnet Freight Rail's performance decline has made rail a less dependable option for time-sensitive automotive cargo, pushing more volume onto the road. The rail reform programme, including private operator access from 2025, may improve reliability enough to make rail a more viable option for some automotive flows over the medium term.

Each of Southern Africa's major ports plays a different role in automotive logistics:

The corridors that connect South Africa's automotive manufacturing base to regional markets are the arteries of the regional automotive supply chain. The N1 north from Johannesburg through Zimbabwe to Zambia carries significant volumes of both finished vehicles and parts. The Trans-Kalahari Corridor serves Botswana and Namibia. The Beira and Nacala Corridors provide access into Mozambique and Malawi.

Border crossing performance on these corridors directly affects the cost and reliability of vehicle distribution into regional markets. The improvements at Beitbridge and the ongoing development of One-Stop Border Posts are directly relevant to automotive logistics operators managing regional distribution.

South Africa's automotive sector is growing in scale and complexity simultaneously. Record export volumes, an expanding regional market, new vehicle brands entering from China, the early stages of EV transition, and the policy opportunities created by AfCFTA all point to increasing demand for automotive logistics capability across Southern Africa.

The logistics providers best positioned to serve that demand are those with genuine end-to-end capability: port handling, bonded storage, inland distribution, cross-border corridor management, and the customs expertise to navigate an increasingly complex trade environment. As the regional automotive market develops, the gap between operators with that capability and those without will become more visible.