Bulk Commodity Freight Cost Drivers: Minerals vs Agriculture in South Africa

June 24, 2026

Read the story

Please submit your details below and one of our logistics experts will reach out within one business day. Thank you.

South Africa moves enormous volumes of bulk freight. Coal, iron ore, and manganese leave the country through dedicated export terminals serving global commodity markets. Maize, citrus, and wheat move through ports and distribution networks that serve both domestic consumers and international buyers.

The logistics infrastructure connecting mines and farms to markets is one of the most important determinants of whether South African producers can compete on price.

But the cost of moving bulk freight is not uniform. Mineral and agricultural commodities have fundamentally different freight profiles, and the cost drivers that affect one sector often work differently in the other. Understanding those differences matters for anyone managing a supply chain in South Africa or planning logistics investment across the region.

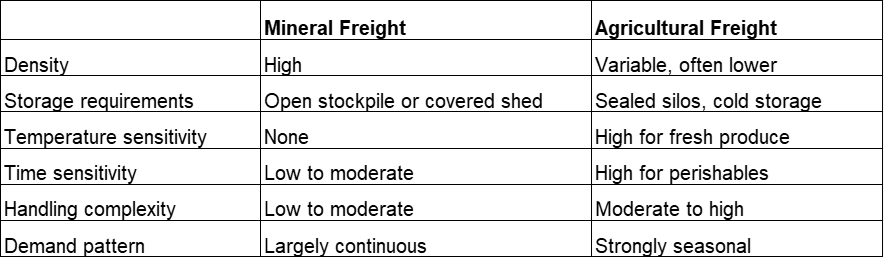

Bulk commodity freight is the movement of unpackaged goods in large quantities. It's just raw material loaded directly into wagons, trucks, or vessel holds and moved in volume. In South Africa, two sectors drive the bulk freight economy: mining and agriculture. Both depend on logistics infrastructure that can shift large tonnages reliably and at a cost that keeps their exports competitive in global markets.

Take bulk logistics out of South Africa's economy, and the export picture collapses. Coal, iron ore, manganese, and chrome are among the country's largest sources of foreign exchange. Maize, citrus, and deciduous fruit are growing in export value and volume.

In both cases, the cost of getting the product from mine or farm to export port is not a secondary consideration. It is one of the primary factors that determines whether South African producers can compete on price in international markets.

That makes the state of South Africa's bulk logistics network a live economic issue. According to the Public Sector Manager, rail freight volumes peaked at 226.3 million tonnes in 2017 and had fallen 34% to 149.5 million tonnes by 2022.

Freight that could no longer move by rail moved by road instead, on infrastructure not built for it, at a cost that worked its way through both the mining and agricultural supply chains.

Coal, iron ore, manganese, chrome, and platinum group metals dominate South Africa's mineral export profile. On the agricultural side, maize, citrus, grapes, wine, and deciduous fruit are among the most significant by volume and value, with the mix shifting year to year depending on harvest conditions and global demand.

The two sectors look very different from a logistics perspective. Mining exports move in consistent volumes along dedicated corridors to purpose-built terminals.

Agricultural exports move seasonally, through shared infrastructure, with handling requirements that vary considerably by commodity. Those differences are reflected directly in how freight costs are structured in each sector.

Mineral bulk cargo is heavy, dense, and largely indifferent to time. Coal and iron ore tolerate outdoor storage in stockpiles. Manganese and chrome can be moved in open wagons without packaging or temperature control. The primary requirements are volume capacity, loading and discharge efficiency, and the ability to move consistent tonnages reliably over long corridors.

The dedicated nature of mineral export infrastructure, the heavy haul rail lines running to Richards Bay and Saldanha Bay, and the bulk terminals at those ports reflect these requirements. The infrastructure is optimized for throughput at scale, and the economics of mineral freight are driven primarily by the cost per ton over long distances.

Agricultural bulk cargo is more varied and more demanding. Grain moves in bulk but requires dry, sealed storage to prevent moisture damage and contamination.

Citrus and other fresh produce require temperature-controlled handling from harvest through to vessel loading. Some agricultural commodities are highly time-sensitive: a consignment of citrus that misses a vessel booking window may arrive at destination in a condition that affects its marketability.

The logistics requirements for agricultural freight, therefore, extend well beyond transport. Storage, conditioning, and handling all form part of the cost structure in a way that does not apply to most mineral commodities.

The comparison below summarizes the key differences between the two freight types:

Mineral freight demand is broadly continuous. Mines produce year-round, and export schedules are driven by production capacity and market demand rather than seasons.

Unlike mining, agricultural freight is seasonal. Demand builds sharply around harvest time and drops away just as quickly. Maize harvests in the Free State and North West provinces create peak demand in the April to July period. Citrus harvests in the Western Cape and Limpopo create a separate peak from June to October.

Those seasonal peaks create capacity pressure at specific ports, on specific rail corridors, and in cold storage facilities. According to the Agricultural Business Chamber's Chief Economist, citing the Crop Estimates Committee, South Africa's 2025-26 summer grains and oilseeds production was estimated at 20.3 million tonnes, near the second-largest harvest on record.

Rail is the most cost-effective mode for bulk freight over long distances when it works. The problem in South Africa is that it has not been working well enough. The shift of bulk freight from rail to road that followed Transnet Freight Rail's decline in performance has added cost across the supply chain. Road freight is more expensive per ton per kilometer than rail, creates road damage that generates further infrastructure costs, and is more exposed to fuel price volatility.

Port shipping costs for bulk cargo are determined by vessel type, route length, and how efficiently the terminal operates. Richards Bay and Saldanha Bay are both purpose-built for high-volume bulk throughput, but their performance depends on what arrives by rail.

When locomotive availability drops and stockpiles run low, vessels arrive to find insufficient cargo ready for loading. The wait time that follows is billed as demurrage, and it falls on the shipper.

According to Transnet's 2023/2024 annual report, rail and port constraints limited iron ore exports to 55 million tonnes in 2023, costing South Africa its position as the world's third-largest iron ore exporter, which it lost to Canada. That is a direct, measurable consequence of infrastructure underperformance on freight cost competitiveness.

The South African government has recognized the scale of the problem. For the 2026 fiscal year, transport has been placed at the center of the government's economic recovery strategy, including a tender for a 25-year concession of the Richards Bay dry bulk terminal and public-private partnerships for dedicated freight corridors.

South Africa's mineral export corridors were built around heavy haul rail. The line from the Northern Cape iron ore mines to Saldanha Bay, operated by Transnet, is one of the highest-capacity heavy haul rail lines in the world. The coal export line from the Mpumalanga coalfields to Richards Bay is similarly dedicated and high-volume. Both corridors are dependent on Transnet Freight Rail's operational performance, and both have suffered from its decline.

Between 2017 and 2022, rail freight volumes dropped by 34%. Locomotive shortages, cable theft, vandalism, and years of deferred maintenance all played a part. The freight that could no longer move by rail moved by road, at a higher cost and on infrastructure not built for it.

The reform picture is improving. Public Sector Manager reports that in August 2025, 11 private train operating companies were conditionally approved to run services on strategic freight routes across six main export corridors.

The additional operators are expected to add 20 million tonnes of capacity per year from 2026/27. That is a meaningful shift, but private operators running new services still need to bed in, and the infrastructure they run on still needs to perform.

Richards Bay handles coal, iron ore, chrome, manganese, and agricultural exports. It is South Africa's largest port by cargo volume and a bottleneck when rail delivery is unreliable. Stockpile levels at the terminal fluctuate with rail performance, which has an impact on vessel scheduling and demurrage costs.

Saldanha Bay is South Africa's dedicated iron ore export terminal, located on the West Coast north of Cape Town. Its performance is tightly linked to the Sishen-Saldanha heavy haul railway. When that line underperforms, iron ore export volumes fall, and the cost per ton exported rises as fixed terminal costs are spread over lower throughput.

At a bulk terminal, loading speed makes a big difference. A vessel on demurrage is costing the shipper money by the hour, and the difference between a smooth loading operation and one interrupted by equipment failure can run to significant sums over a single vessel call.

Reclaimers, conveyors, and ship loaders all need to be available and performing when a vessel is alongside. When they aren't, the vessel waits, and the clock runs. Equipment maintenance at South Africa's bulk terminals has suffered from the same underinvestment that affected the rail network, and the cost has been borne by exporters in the form of demurrage charges that should have been avoidable.

Agricultural freight rates move with the seasons. When citrus volumes build through June to October, reefer containers become scarce, and rates climb. When the maize harvest coincides with competing demand for bulk vessel capacity, booking windows tighten and the cost of securing space goes up.

South Africa's agricultural exporters have identified higher fuel prices, rising shipping costs, and logistical challenges in key export markets as major concerns heading into 2026. Citrus faces an additional squeeze: South American producers are bringing higher volumes to the same markets at the same time, putting pressure on both pricing and the logistics capacity available to service those shipments.

Grain storage in South Africa runs through commercial silo networks, mostly at inland collection points close to production areas. The cost of moving grain in, storing it monthly, and moving it out again adds up before the cargo has even reached a port. When silos fill up at harvest time, storage costs rise, and the pressure to push grain through to export terminals early can create congestion further down the chain.

Fresh produce is a different problem. Cold chain infrastructure, from pack house through transit storage to port facilities, is expensive to run and tight on capacity during peak export periods. South Africa's citrus industry has invested heavily in its own cold chain, but the pinch points at port during the June to October window are a recurring feature of the logistics calendar rather than an occasional exception.

For fresh produce, time is money in a direct and unambiguous sense. A consignment of citrus or grapes that misses its vessel booking faces a choice between waiting for the next available vessel, with the associated storage cost and risk of quality deterioration, or being rerouted at a higher cost to reach the market within the quality window.

The cost of this time sensitivity is reflected in the premium that fresh produce exporters pay for reliable vessel scheduling, reefer container availability, and port handling that does not add unnecessary days to the supply chain. It is also reflected in the cost of logistics failures: a claim for quality deterioration on a reefer shipment can exceed the freight cost many times over.

Many of South Africa's agricultural production areas are distant from the rail network and dependent on roads for the first leg of the journey to a silo, pack house, or port. The condition of rural roads in key agricultural provinces is variable, and the cost of moving bulk grain or fresh produce from farm to collection point can represent a significant proportion of total logistics cost.

Rail reform that extends rail access to agricultural corridors, improving the economics of moving grain from inland silos to export ports by rail rather than road, would have a material effect on the cost competitiveness of South African agricultural exports. Farms located near rail sidings already benefit from lower inland logistics costs, and the extension of those benefits to a broader area of production would be commercially significant.

The freight cost structures of South Africa's mineral and agricultural sectors are shaped by different infrastructure dependencies, different demand patterns, and different handling requirements. What they share is exposure to the performance of Transnet's rail and port network, which remains the single most important variable in the cost competitiveness of South African bulk exports.

The reform programme underway, including private sector access to rail corridors and the concession of bulk terminal infrastructure, is directly targeted at the constraints that have been adding cost to both sectors. The pace of implementation will determine how quickly those benefits flow through to exporters and the logistics operators that serve them.