What Freight Data Should You Get from a Logistics Provider?

July 31, 2026

Read the story

Please submit your details below and one of our logistics experts will reach out within one business day. Thank you.

International trade relies on a network of rules and fees that ensure goods move across borders legally and fairly. Among these, duties, tariffs, and taxes are three of the most important, as well as often being misunderstood.

Knowing the difference between them is essential for importers, exporters, and logistics professionals alike. Each plays a specific role in determining the true cost of moving goods, and knowing how they work can help businesses plan better, avoid delays, and make more informed pricing decisions.

While the terminology can be confusing, these charges serve distinct purposes. This article explains what each term means, how they are calculated, and why they matter to global supply chains.

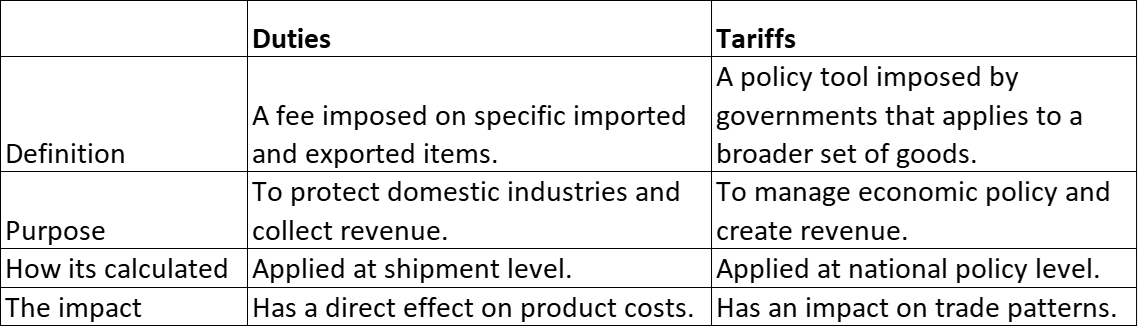

Duties are imposed by governments on imported and exported goods to regulate trade and protect domestic industries, as well as to generate revenue. In logistics, these are often called customs duties as they are collected by the customs authorities when goods enter a country.

The purpose of duties is:

1. To protect local producers by making imported goods slightly more expensive.

2. And to generate income for the government through cross-border trade.

The rate of duty on a product depends on several factors, including:

• The type of product: Goods, like textiles, alcohol, or electronics, hold higher duties than goods like basic foods or pharmaceuticals.

• The value of the goods: Duties are often calculated as a percentage of the declared value.

• The country of origin: Trade agreements or regional blocs can influence the duty rate.

For example, a shipment of electronics imported into South Africa may face a 20% duty, while agricultural goods imported from within the Southern African Development Community (SADC) might qualify for reduced or zero duties due to preferential trade terms.

Every product traded internationally has a classification code under the Harmonized Tariff Schedule (HTS). These codes determine the applicable duty rates.

Factors that influence duty rates include:

• HTS Code Classification: Accurate classification ensures the correct rate is applied.

• Trade Agreements: Preferential or free trade agreements (FTAs) often reduce or eliminate duties between member countries.

• Import Quotas: When a certain volume limit is exceeded, duties may increase to control import levels.

For example, under the African Continental Free Trade Area (AfCFTA), many goods traded between African nations benefit from lower or zero duty rates, making accurate classification important to understand for the specific goods shippers are importing and exporting.

While duties and tariffs are closely related, they are not the same thing.

A tariff is a general tax or fee that has been imposed by a government on imported goods. This is essentially a type of duty. However, the specific term “tariff” is broader and more related to trade policies, rather than for individual shipments.

Tariffs can also be protective, designed to support domestic industries by making importing products from elsewhere more expensive and therefore discouraging those imports. Tariffs can also be a source of revenue and are usually aimed at increasing income for the government.

An example we can look at is a common tariff applied to imported vehicles. Countries that have a strong domestic car industry often impose higher import tariffs, sometimes up to 25%, to directly encourage local manufacturing. It’s common to adjust tariffs on other products in response to the global market and how it fluctuates, or how trade negotiations change. Some of these are commonly steel and textiles.

Unlike duties, which are calculated per shipment, tariffs are established through national or international trade policies. They are typically determined as a percentage of the goods’ declared customs value.

For importers, the tariff cost is generally calculated as:

Tariff = (Declared Customs Value) × (Tariff Rate%)

For example, if an importer brings USD 50,000 worth of machinery subject to a 10% tariff, the tariff amount payable would be USD 5,000.

In short, duties are transactional, while tariffs are policy-driven.

On top of duties and tariffs, import taxes are another layer of charges that importers must be aware of to not be affected by surprising costs. Import taxes are typically applied to goods entering a country and are separate from customs duties and tariffs. Import taxes help recover costs related to domestic consumption.

The most common types of import taxes include:

• Value-Added Tax (VAT): Charged on most goods and services, calculated as a percentage of the total landed cost (which includes duties and freight).

• Goods and Services Tax (GST): This is similar to VAT and is only used in some markets like Canada and Australia.

• Excise Taxes: Applied to specific products such as fuel, alcohol, or tobacco.

For example, a business importing spirits into Botswana may pay customs duties, import VAT, and an excise tax. Each is calculated differently and serves a unique purpose.

The key steps of calculating duties and taxes include:

1. Classifying the product using the correct HTS code.

2. Determine the customs value, including cost, insurance, and freight (CIF).

3. Apply applicable duty and tariff rates based on the elements mentioned above.

4. Add import VAT or other taxes based on the total landed cost.

For instance, if a shipment valued at USD 100,000 has a 10% duty and 15% VAT, the total duty is USD 10,000, and VAT applies to USD 110,000 — making the total payable USD 26,500.

Misclassification or under-declaring values can result in fines, shipment delays, or even seizure of goods.

The total landed cost represents the full expense of getting goods to their final destination. This includes:

• Product cost

• Shipping and insurance

• Customs duties and tariffs

• Import taxes (VAT, excise, or sales tax)

• Handling and storage fees

Calculating landed cost accurately helps importers understand profit margins and avoid unexpected expenses once goods arrive.

Once goods have been imported to a country, there may also be an applicable sales tax. This is usually a national or regional tax on the sale of goods and services and is added at the point of sale.

For logistics, sales tax affects how companies can account for the landed costs and set pricing. Sales tax is not charged during customs clearance like tariffs; instead it becomes part of the overall tax once goods are locally distributed.

The entity legally responsible for ensuring all duties, tariffs, and taxes are paid for is the Importer of Record (IOR), which every import needs. The IOR is responsible for making sure that documentation such as the bill of lading, commercial invoices, and packing lists is up to date and correct. It’s also the responsibility of the IOR to register for VAT to ensure compliance with local tax laws and prevent shipping delays and penalties.

The Certificate of Origin (COO) verifies where goods were produced and can significantly impact duty rates. Due to preferential origin, goods that have been produced in countries with trade agreements may qualify for reduced duties, whereas those goods that are imported without those trade benefits face the standard duties.

For example, agricultural exports within the Southern African Development Community often qualify for duty exemptions under regional trade agreements, while similar goods imported from outside Africa may attract standard or higher rates.

International Commercial Terms are standardized rules that define the responsibilities of buyers and sellers in global trade. They outline those who handle shipping, insurance, and import and export duties.

Common Incoterms include:

• EXW (Ex Works): The buyer takes on most responsibilities from the seller’s facility.

• CIF (Cost, Insurance, and Freight): The seller covers costs up to the destination port.

• DDP (Delivered Duty Paid): The seller pays all duties and taxes, delivering the goods ready for unloading.

• DDU (Delivered Duty Unpaid): The buyer pays duties and taxes upon arrival.

Understanding Incoterms helps importers and exporters clarify expectations and avoid costly misunderstandings during transit.

Understanding duties, tariffs, and taxes is a core part of efficiently managing global logistics. When mistakes are made with classification or cost calculations, unexpected expenses and delayed deliveries can happen.

Integrated logistics providers like Reload Logistics support clients in streamlining multimodal transport and coordinating cross-border operations to make sure goods reach their destinations on time.

By staying informed and planning ahead, businesses can turn regulatory complexity into a competitive advantage, building smarter, more resilient supply chains.

Import duty is a fee charged on goods entering a country, while taxes are added costs related to domestic consumption.

No. Duties apply to imports or exports, while taxes are broader fees charged on goods and services.

It’s a customs fee applied by governments on imported goods to protect domestic industries and generate revenue.

The Importer of Record (IOR) is responsible for paying import duties and taxes.

By classifying goods with the correct HTS code, determining customs value, and applying the relevant duty and tax rates.